In summary

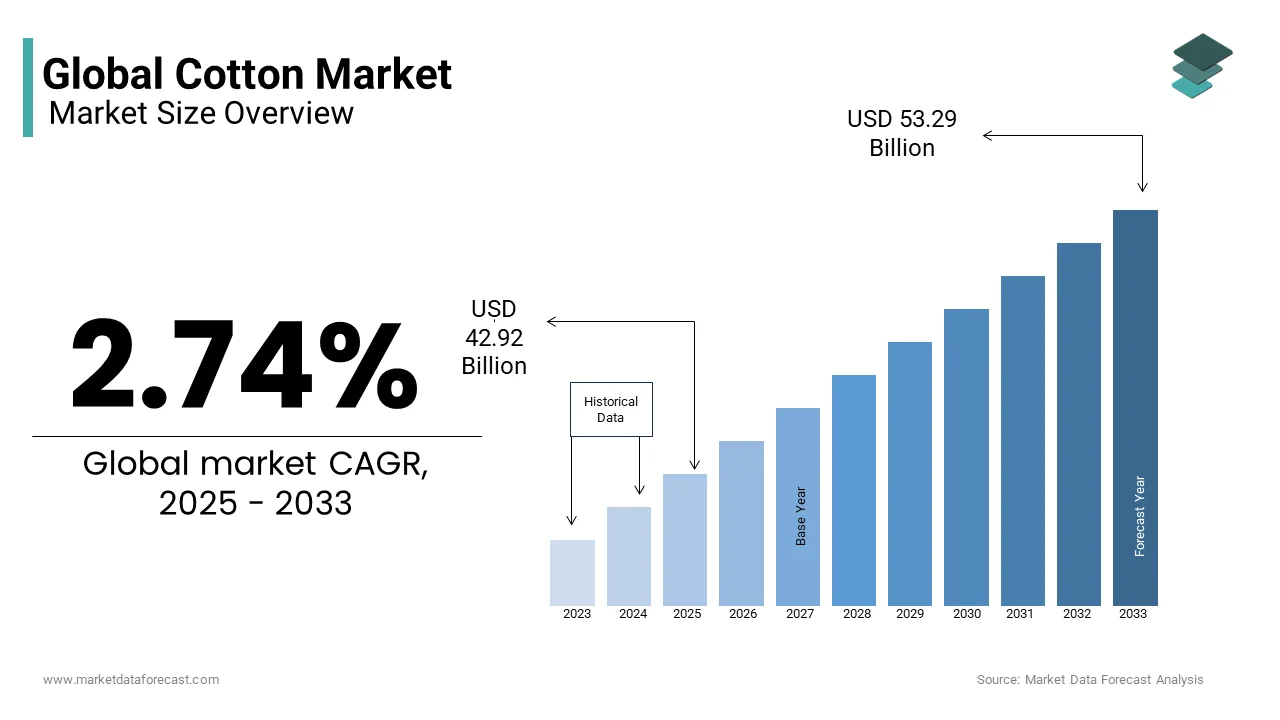

- Africa’s cotton production is experiencing a rebound in 2025, the market is projected to reach $6.36 billion, with a further increase to $8.08 billion by 2030, according to Mordor Intelligence.

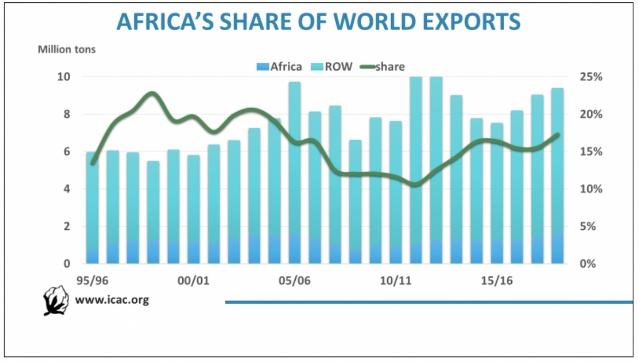

- Africa’s share in world cotton trade is expected to grow to 16% by the end of 2025, with exports reaching over 1.4 million tons.

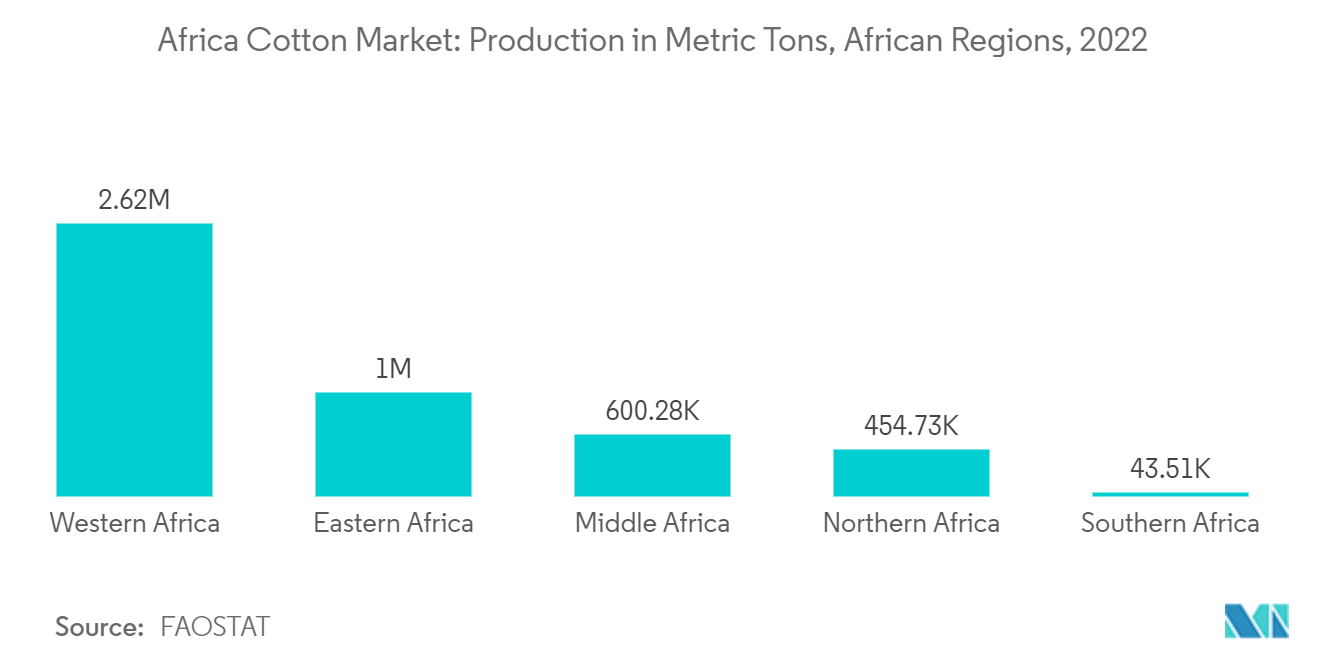

- The production of cotton in Western Africa, Middle Africa, Northern Africa, Southern Africa, and Eastern Africa is 2,617,129 metric tons, 600,275 metric tons, 454,731 metric tons, 43,513 metric tons, and 1,000,643 metric tons, respectively. Thus, Western African countries lead the production of cotton.

Deep Dive!!

Cotton remains one of Africa’s most strategic agricultural commodities. Over the years, it has helped in shaping rural livelihoods, export earnings, and industrial ambitions across the continent.

However, reports indicate that the sector is navigating a delicate balance between opportunity and vulnerability. While the resilient production systems in West Africa sustaining high output despite erratic rainfall and global price headwinds, other regions wrestle with structural bottlenecks, climate shocks, and shifting policy signals.

The latest U.S. Department of Agriculture (USDA) cotton projections for 2025/26 (August–July) indicate that world cotton production will decrease by 1.5 million bales (1 percent) to 118.4 million bales but remains the second highest total since 2017/18. The report also revealed that Africa’s top ten producers collectively account for more than 6.3 million 480-lb bales, anchored by a handful of highly organized national systems that combine coordinated input supply, ginning capacity, and price support mechanisms.

Yet beneath these headline volumes lies a complex story of institutional strength, market exposure, and economic dependence. For some countries, cotton is the largest non-mineral export and a primary source of rural cash income; for others, it is a high-value niche crop tied to premium textile and garment production.

In this article, we take a deep dive into the top 10 cotton producers in Africa in 2025 to enable us understanding who leads the fields, and why. This overview offers a window into the interplay of policy, agronomy, and trade shaping Africa’s agricultural future.

10. Chad

Chad’s cotton outlook for 2025/26 sits around 150,000 bales on approximately 165,000 hectares, with yields nearing 198 kg/hectare. This is below the five-year norm and far off the record 2016/17 yield, which was approximately 242 kg/hectare. Despite large planted areas, production has been affected by heavy exposure to rainfall variability, and persistent pest pressure. Official reports highlight both the long-run downshift in yields and the bounce-back potential when weather and logistics cooperate.

The value chain of cotton production in Chad remains organized around Cotontchad, a company which aggregates seed cotton, provides input credit, and operates the gins. Structurally, it functions as the system’s hinge that handles the coordination of inputs, collection timetables, and export sales, much like other Francophone cotton systems. Public documentation shows Cotontchad working with smallholders in southern provinces and (historically) operating in a dominant/monopoly role. That concentration helps with logistics in a vast, infrastructure-poor country, but it also means working-capital tightness or ginning bottlenecks can suppress realized output relative to area sown.

In the past, a cotton price-stabilization fund (CSPC) cushioned farm-gate prices in the countru, but the mechanism was dismantled in the early 1990s, leaving producers more exposed to world-price swings. Today, the resilience agenda leans on climate-smart, landscape-level efforts of some private initiatives that are piloting regenerative practices, better water/soil management, and farmer-organization capacity across the seven provinces.

9. Zimbabwe

The 2025/2026 USDA report pegs Zimbabwe’s lint output at approximately 225,000 bales, broadly unchanged in planted area from the prior season. In the same vein, domestic figures from the Agricultural Marketing Authority point to approximately 63,000 tonnes of seed cotton for the 2025 marketing year, a rebound from the sharply reduced 2024 crop that was cut by drought conditions linked to an El Niño pattern. This year-on-year volatility is not unusual in Zimbabwe’s cotton belt (comprising of Masvingo, Gokwe, and the Zambezi Valley) where rainfall variability is extreme and most smallholder plots are rain-fed. In stronger years with timely rain, deliveries have been known to double, underscoring the elasticity of production to climate.

In Zimbabwe, the Presidential Inputs Scheme remains the central policy tool for sustaining smallholder engagement in cotton. Under this program, farmers receive seed, fertiliser, and pesticides on credit, repayable through seed cotton deliveries to the ginning companies, primarily the state-linked Cotton Company of Zimbabwe (COTTCO). COTTCO’s role is twofold: coordinating out-grower finance and pushing quality upgrades, especially contamination control and improved picking practices. Evidence from equityaxis.net reports shows that when input packages are fully funded and distributed ahead of planting, output responds quickly, proving that productivity constraints are not purely biophysical but also logistical and financial.

Locally, cotton is a key cash crop for over 350,000 rural households and a relevant, though not dominant, export earner. It injects liquidity into low-income districts where alternative cash crops are limited, helping households pay for school fees, staple grain, and basic goods. On the macro side, lint exports contribute to foreign currency earnings, though the sector’s share has diminished relative to tobacco and minerals. Consistent field-level productivity improvements, contamination reduction, and investment in irrigation for high-potential zones could buffer Zimbabwe’s cotton economy against the climate and price shocks that have defined the last decade.

8. Egypt

Although Egypt’s cotton sector is heading for a smaller harvest in 2025/26, it remains one of the top producers in the continent. Government and USDA data point to production between 250,000 and 320,000 bales, well down from recent highs, as farmers cut plantings after 2024/25 left unusually large stocks unsold. Most of the crop still comes from the Nile Delta, especially Al Buhayrah, Ash Sharqiyah, and Kafr ash Shaykh, where conditions are ideal for Egypt’s famous long-staple varieties. But even with strong ginning capacity and a world-class reputation, Egypt’s volumes remain far below West Africa’s leaders.

According to experts, the downturn is partly policy-driven. In 2024/25, official auction prices for seed cotton more than doubled from the previous year. While this looked attractive on paper, it put off private buyers, slowed local purchases, and created an inventory overhang. This in turn discouraged farmers from planting as much in 2025/26, shrinking harvested area from around 130,000 hectares to about 80,000 hectares. It’s a textbook case of how high prices without matching demand can backfire on production.

Even with smaller harvests, cotton still plays a big role in Egypt’s economy, just in different ways. Premium Giza lint earns top dollar on global markets, and the domestic textile and garment industry is expanding fast. In early 2025, ready-made garment exports jumped 24% to $812 million in Q1, while textile exports topped $493 million in the first five months. Mills are running at their highest consumption in 14 years, which means more lint is being imported when local supplies run short. In short, Egypt’s strength lies in quality, branding, and manufacturing, and smart policy could protect its niche even as volumes stay modest.

7. Nigeria

Nigeria is expected to produce about 350,000 bales of cotton in the 2025/26 season, grown on roughly 270,000 hectares. According to reports, yields in the country remain low, averaging 0.28 tonnes per hectare, and haven’t improved much from last year. While this keeps Nigeria just ahead of Egypt in output, it’s far below the country’s golden years of the 1970s–80s, when production sometimes topped 700,000 bales and cotton was a leading non-oil export. Most of today’s cotton comes from the northern states of Kano, Katsina, Kaduna, Zamfara, and parts of Borno, where conditions are good for growing the crop but expansion is held back by erratic rainfall and security challenges.

The industry’s problems are well known. Farmers often work with poor-quality seed, face damaging pest outbreaks, and have unreliable access to credit and inputs. Programs like the Anchor Borrowers Programme and support from the National Cotton Association of Nigeria have tried to boost the sector by providing seeds, fertilizer, and guaranteed markets. However, these efforts can be inconsistent, with farmers reporting late deliveries and slow payments. Without steady farm-gate prices and cash-ready ginneries, many farmers switch to other crops like maize or groundnut when cotton’s profits look shaky, keeping yields and output stuck in a cycle of underperformance.

Even with its smaller footprint, cotton is still important to Nigeria’s economy. It supports 200,000–250,000 farming households and supplies lint to a domestic textile sector that wants to grow but often has to rely on imports from Benin, Chad, and beyond. If Nigeria could raise production to 500,000–600,000 bales, it would cut import costs, save foreign exchange, and create more jobs in spinning, weaving, and garment-making. Achieving this would require better seed systems, widespread pest management, and stronger contracts between farmers and ginners, which are steps that could help cotton reclaim its place as a key non-oil export and driver of industrial growth.

6. Tanzania

Tanzania’s cotton industry is set to bounce back in the 2025/26 season, with production expected to reach around 400,000 bales, up from 350,000 bales in the 2024/2025 season. This recovery is helped by better weather; but yields, at roughly 198 kg/hectare, are still below what could be achieved with timely pest control and input delivery. Cotton growing is concentrated in the western zone regions like Shinyanga, Mwanza, Geita, Simiyu, and Mara, where smallholder farmers working 1–2 hectare plots dominate. In good years, like 2019/2020 when favourable rains and early input distribution helped produce 594,000 bales, the sector shows its potential. But weather shocks and pest outbreaks have kept output unpredictable.

The Tanzania Cotton Board (TCB) plays a central role in regulating the sector. It licenses buyers, sets and announces farm-gate prices, and ensures grading standards. Strong price communication and fair competition among ginners keep farmers engaged, but delays in supplying subsidized pesticides or weak extension services can quickly dent yields, leaving crops vulnerable to pests like bollworm and jassid. Another key factor is the financial strength of buyers: when ginners have cash ready, buying is smooth; when they don’t, farmers may switch to other crops like maize or sunflower in the next season.

Cotton is Tanzania’s second-largest cash crop by export volume after cashew, supporting over 500,000 farming households and thousands more in ginning, transport, and port jobs. Most lint is exported to Bangladesh, India, and China, generating crucial foreign exchange for a country with a persistent trade deficit. Locally, the textile industry is small but growing, backed by the Tanzania Industrialization Strategy 2025, which aims to boost spinning and weaving capacity. If 2025 brings good rains and timely input delivery, production could rise to 450,000–500,000 bales, improving incomes and export earnings. But late inputs or drought could drop output closer to the five-year average of ~319,000 bales, tightening both rural cash flow and the national export balance.

5. Burkina Faso

Burkina Faso’s cotton industry is settling at around 610,000 bales in the 2025/26 season, grown on roughly 360,000 hectares with yields close to 369 kg/hectare. While this is far from the record 1.31 million bales of 2016/2017, it’s a recovery from the low point of 2022/2023. The improvement is mainly due to stabilized planting areas and slight gains in efficiency. Two big hurdles remain however, which are ongoing security challenges in parts of the east and center, which can keep farmers from accessing their fields, and input delivery issues, such as fluctuating fertilizer prices mid-season and late arrivals, that were especially disruptive in 2024/25.

The cotton value chain is dominated by three main players, which are SOFITEX (about 80% of production), SOCOMA, and FASO COTON (sharing the remaining 20%), with SOFITEX alone operating over 15 gins. This setup allows for coordinated input credit, collection, and export sales, but it also means that any operational or cash flow problem in a few key companies can ripple across the whole sector. A turning point came in 2016, when Burkina phased out some producers after persistent penalties for lower fiber quality, shorter staple length and weaker ginning performance. The losses were significant, and since then the industry has been working to rebuild its reputation in global markets for premium-quality lint.

Cotton, alongside gold, is one of Burkina Faso’s most important export earners. In 2020, it represented about 47% of agricultural export revenues and continues to inject cash into rural economies, supporting jobs in farming, ginning, and transport. Even though world cotton prices dropped by roughly 10% in late 2024, the government kept farm-gate prices steady to encourage planting. The sector’s future growth depends on three main levers: better seed quality and pest control to raise yields, improved security and logistics to expand planted and harvested areas, and maintaining high lint quality to secure strong export prices. If these align, production could return to 700,000–800,000 bales in the next few seasons, strengthening Burkina Faso’s foreign exchange earnings and rural livelihoods.

4. Cameroon

Cameroon’s cotton industry is one of the best-organized in West and Central Africa, producing around 650,000 bales in the 2025/26 season from roughly 230,000 hectares. While this is a drop from the record 740,000 bales in 2023/24, yields remain high at 615 kg/ha, well above most African averages. Cotton is grown mainly in the Far North, North, and Adamawa regions by smallholder farmers, most with less than one hectare under the coordination of SODECOTON, which works with over 200,000 producers. This coordination ensures timely input delivery, efficient collection, and consistent ginning, giving Cameroon a unique advantage in the region.

SODECOTON is the backbone of Cameroon’s cotton success. In mid-2025, the government expanded its ownership to about 89% by acquiring a major private shareholder’s stake, strengthening state control over pricing, input-credit cycles, and investments in ginning and oil processing facilities. The export market is strong and diverse, as China alone buys nearly 38% of Cameroon’s lint exports, followed by Bangladesh, Vietnam, and Indonesia, helping cushion against price fluctuations. The Bank of Central African States (BEAC) projects seed cotton production to reach 350,100 tonnes in the 2024/2025 season (roughly 720–760k bales), showing resilience even in a year of slightly lower yields.

Cotton is vital to the northern regions of Cameroon, supporting the livelihoods of nearly 2 million people directly and indirectly, from farming to ginning to transport. It’s also an important driver of the national economy, with the World Bank recently highlighting that cotton, along with cocoa and improved electricity supply, as key contributors to Cameroon’s 3.5% GDP growth in 2024. In a country where nearly 40% of people live below the poverty line, the seasonal income from cotton sales helps families pay school fees, cover health costs, and buy food. Going forward, the sector’s growth will depend more on improving yields than expanding land, with priorities including timely inputs, pest control, maintaining seed quality, and reducing contamination from field to gin. If these are sustained and Asian demand remains strong, Cameroon is well-positioned to keep its position as one of the top cotton producers in Africa, and continue boosting rural incomes and foreign exchange earnings.

3. Côte d’Ivoire

Côte d’Ivoire’s cotton production is on track to reach 745,000 bales in 2025/2026, grown on about 375,000 hectares with yields averaging 433 kg/hectare. This marks a strong recovery from the 2022/2023 slump, when yields collapsed to just 236 kg/hectares due to pest outbreaks and poor field conditions. The rebound is credited to improved farming practices, better pest control, and more reliable input distribution. This steady climb from 660,000 bales in 2024/2025 to 745,000 bales keeps Côte d’Ivoire ahead of Cameroon and Burkina Faso in production, confirming its spot among Africa’s top cotton producers.

The Conseil du Coton et de l’Anacarde (CCA) has played a key role in stabilizing the sector. For 2025/2026, it kept producer prices unchanged at 310 CFA/kg for first-grade and 285 CFA/kg for second-grade cotton, backed by a direct subsidy of 44 CFA/kg and approximately 18,000 CFA/hectare to help offset fertilizer and insecticide costs. These measures protect farmer incomes, encourage consistent planting, and help co-operatives secure inputs on time crucial in a smallholder-driven system. Such price stability is especially important after recent volatility, giving farmers the confidence to invest in their fields.

Cotton is almost entirely export-driven in Côte d’Ivoire, with 735,000 bales expected to be shipped in 2025/2026, mostly to Asian markets like Pakistan and China. Over 90% of Ivorian lint goes to Asia, meaning that global price shifts in those markets can quickly affect local cash flow. Domestic spinning is minimal, with local consumption at just approximately 10,000 bales, so cotton’s biggest contributions are foreign exchange earnings and rural liquidity, particularly in the northern regions where it is a major cash crop. The sector is supported by more than 500 producer co-operatives, which are working to improve seed quality and maintain high fiber standards. While weather patterns and pest flare-ups remain the main risks, strong co-op networks, steady pricing, and reliable input supply keep Côte d’Ivoire well-positioned to maintain its lead over mid-tier producers and challenge the top two in good years.

2. Benin

Benin has cemented its position as one of Africa’s top two cotton producers, turning out between 1.20 and 1.26 million bales in 2025/2026 from about 535,000 hectares. Yields have held steady at 0.49–0.51 tons per hectare, and over the past five seasons, output has averaged approximately 1.27 million bales, a rare streak of stability in a region where weather shocks and logistical hiccups often disrupt production. Benin’s success isn’t down to unusually favorable conditions, but to disciplined management: well-timed planting, efficient input delivery, and strong oversight ensure that what gets planted actually makes it to market.

The sector’s stability rests on the Association Interprofessionnelle du Coton (AIC), a powerful coordination body that brings together farmers, ginners, and input suppliers under one umbrella. Since its formal launch in 1999, the AIC has handled seed production, extension services, quality control, and negotiations with the government. For 2025/2026, the state set farm-gate prices at 300 CFA/kg for first-grade and 250 CFA/kg for second-grade cotton, while also capping fertilizer prices; NPK at 17,000 CFA and urea at 15,000 CFA, to protect farmers’ margins. This combination of price stability and reliable supply chains reduces the temptation for side-selling and keeps production consistent even when global lint prices dip.

Cotton remains a pillar of Benin’s economy, accounting for around 70% of agricultural export value and forming, alongside cashew, more than a third of total goods exports. The seasonal cash flow from cotton sales supports hundreds of thousands of smallholder households in the north and helps maintain foreign exchange reserves. Now, Benin is aiming to keep more value at home. Through the Glo-Djigbé Industrial Zone (GDIZ), the country is investing in spinning, weaving, dyeing, and garment-making to shift from exporting raw lint to finished products. If even a fraction of the approximate 300,000 tons of lint currently exported were processed domestically, it could significantly boost GDP and create jobs. Still, success depends on three near-term factors like affordable fertilizer, timely and pure seed distribution, and a favorable global price environment for lint. Benin’s well-oiled system gives it resilience, but not immunity, to the challenges facing African cotton.

1. Mali

Mali is once again Africa’s top cotton producer, with approximately 1.30 million bales expected in the 2025/2026 season from about 700,000 hectares of farmland. This marks a clear rise from approximately 1.07 million bales the year before and comfortably beats the five-year average. The setbacks of the pandemic years and the pest-hit 2022/2023 season are now behind, as both planted area and yields have bounced back to the country’s best range of 0.40–0.43 tons per hectare. Reports also show that farmers are expanding plantings by roughly 50,000 hectares this season, signaling renewed confidence in the crop.

At the heart of Mali’s cotton success is the Compagnie Malienne pour le Développement du Textile (CMDT), the state-controlled body that oversees input supply, extension services, ginning, and exports. In February 2025, CMDT secured a CFA 150 billion loan from local banks to fund seeds, fertilizers, logistics, and timely payments to farmers, which is crucial for maintaining grower trust. Government policy also plays a big role: farm-gate prices were raised to 300 CFA/kg in 2024/25, and subsidies for both fertilizer and purchase prices continue to encourage production. These measures have been key to reviving output after the steep drop in 2020/21.

Cotton is Mali’s most important agricultural export and a lifeline for rural communities in the south. It ranks just behind gold in export earnings, supporting hundreds of thousands of farming households and creating millions of related jobs in ginning, transport, and trade. In some years, cotton has contributed around 11% of export value and a significant share of GDP. When production falters due to pests, poor rains, or delayed inputs, both the country’s foreign exchange reserves and rural living standards take a hit. For now, Mali’s outlook is strong; with solid institutions, guaranteed financing, and attractive prices, the country is well-positioned to maintain its number-one spot till the end of the 2025/2026 season, provided the weather cooperates and pest outbreaks stay under control.

https://www.africanexponent.com/top-10-cotton-producers-in-africa-2025/