In Summary

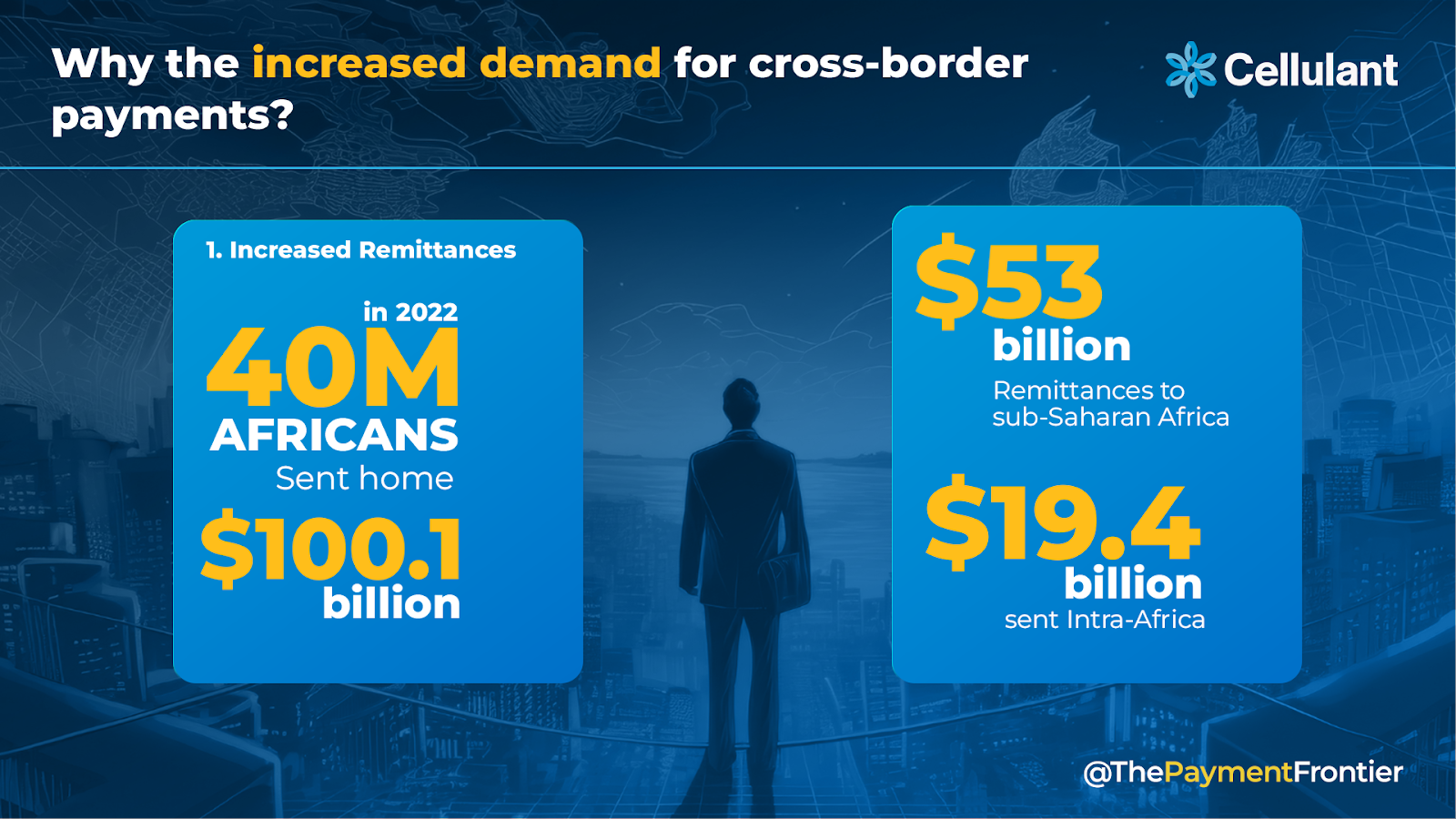

- With over $95 billion in remittances in 2024, Africa remains one of the largest recipients of remittance flows globally, contributing significantly to household income and GDP in countries like Nigeria, Kenya, and Ghana.

- Top-performing startups like LemFi, NALA, Flutterwave, and Chipper Cash are now processing billions in cross-border transactions monthly, with LemFi alone handling over $1 billion/month and over 1 million active users.

- Mobile wallet penetration and fintech adoption are driving growth, with startups reducing transfer fees from 7–12% down to 1–3%, making remittances more affordable for diaspora communities.

- The digital remittance market in the Middle East and Africa is expected to reach $4.6 billion by 2030, growing at 17.4% CAGR, highlighting the scalability of Africa-based solutions.

Deep Dive!!

Africa’s remittance landscape is undergoing a profound transformation, driven by a surge in digital innovation and the emergence of homegrown fintech startups. The continent, which received over $95 billion in remittances in 2024, is now witnessing a paradigm shift as local companies challenge traditional global players like Western Union and MoneyGram. This influx of funds not only supports families but also fuels economic development, with remittances accounting for a significant portion of GDP in several African nations.

At the forefront of this revolution are startups such as LemFi, NALA, and Sendwave, which are leveraging technology to reduce transfer costs and enhance accessibility. For instance, LemFi has expanded its operations across Europe and North America, processing over $1 billion in monthly transactions and securing a $53 million funding round in early 2025. Similarly, NALA has facilitated over $1 billion in remittance transfers to Africa and Asia, demonstrating the scalability of African fintech solutions.

In this article, we delve into the top 10 largest money remittance startups in Africa as of 2025, examining their growth trajectories, technological innovations, and the impact they are making on the global remittance market. As the digital remittance market in the Middle East and Africa is projected to reach $4.6 billion by 2030, with a compound annual growth rate of 17.4% from 2025 to 2030, these startups are not only reshaping financial inclusion but also positioning Africa as a formidable player in the global fintech arena.

10. Nsano – Ghana

Nsano Ltd, a Ghanaian fintech company founded in 2013, has emerged as a leading mobile money and remittance aggregator in Africa. Headquartered in Accra, Nsano has expanded its operations across multiple African markets, including Ghana, Rwanda, Zambia, Côte d’Ivoire, and the United Kingdom. The company facilitates seamless digital payments across over 30 countries, connecting businesses and governments to various African markets.

In early 2025, Nsano made significant strides in its expansion by securing two key licenses from the National Bank of Rwanda, under the Payment Aggregation and Payment Remittances Service Licenses (Category II and III). This move underscores the company’s commitment to enhancing financial inclusion and providing secure payment solutions across the continent.

A pivotal development in Nsano’s growth trajectory was its strategic partnership with Arab Financial Services (AFS) in February 2025. This collaboration aims to transform card payments in Africa by integrating AFS’s state-of-the-art card processing services into Nsano’s existing mobile money infrastructure. The partnership enables Nsano to offer Visa and Mastercard processing, including both issuing and acquiring services, to financial institutions and merchants across the region. Under the leadership of CEO Priscilla Hazel, Nsano continues to innovate and expand its services, positioning itself as a key player in Africa’s fintech landscape. With a focus on secure and scalable payment solutions, Nsano is poised to redefine the fintech landscape in East Africa and beyond.

9. Grey – Nigeria

Grey (formerly Aboki Africa) has fast-matured from a niche fintech for digital nomads into one of Africa’s most visible cross-border payments platforms. The startup, founded in 2020 and accepted into Y Combinator’s Winter 2022 batch, secured a $2M seed round that jump-started product development and regional expansion. By August 2024 Grey publicly celebrated passing the 1-million user milestone, a clear signal of product-market fit among freelancers, remote workers and small businesses that need low-friction foreign bank accounts, multi-currency wallets and instant FX.

Technically Grey’s proposition combines virtual foreign bank accounts, instant currency conversion and cross-border payouts, features that directly attack traditional pain points (costly FX, slow transfers, limited payout rails) for Africa’s diaspora and gig economy. The company has broadened its footprint beyond West Africa into East Africa, LATAM and Southeast Asia; strategic integrations (for example with regional processors) have helped Grey introduce more payout channels and USD-denominated flows for users. Those moves, plus a brand refresh and a sharpened global positioning explain why investors and partners view Grey as a scalable remittance/FX layer rather than just another payments app.

But scaling cross-border FX and remittance services in Africa is capital-intensive and compliance-heavy. Grey’s path forward hinges on three business realities; securing deeper liquidity lines and competitive FX rates, expanding regulated payout licenses in target jurisdictions, and sustaining trust through strong AML/CFT controls as it grows volumes. If Grey can keep improving unit economics while navigating licensing and FX volatility, it stands to retain leadership among remittance startups serving the continent’s gig economy, turning the 1-million user milestone into a durable commercial advantage.

8. Eversend – Uganda

Eversend has evolved from a Kampala startup into one of Africa’s best-known “neobank” challengers, a multi-currency wallet, FX engine and cross-border payouts layer that stitches together mobile-money rails across multiple markets. Launched in 2017, the platform markets itself as a one-stop hub for Africans and the diaspora to hold, exchange and move funds in local and hard currencies; its product set now includes multi-currency wallets, USD/EUR virtual accounts, card issuing, wholesale FX and B2B payout APIs that let merchants and platforms pay out to mobile money and bank accounts across the continent. This product breadth positions Eversend not just as a consumer remittance app but as a payments infrastructure provider for businesses expanding into Africa.

Commercial traction has been driven by two connected advantages: lower end-user fees and rails that convert between mobile money and bank rails in real time. Eversend’s blog and product pages emphasise near-instant transfers to key markets (Kenya, Uganda, Ghana and Nigeria), competitive wholesale FX, and the roll-out of USD/EUR virtual bank accounts to help users receive international payments, features that directly address pain points for freelancers, SMEs and diaspora recipients. Market intelligence platforms also list Eversend among scaled African fintechs with meaningful capital and investor backing, noting its ambition to serve both retail remittances and B2B payment flows. CEO Stone Atwine has repeatedly framed Eversend’s mission as “making cross-border money movement as seamless and affordable as local transfers,” a pitch that resonates with both retail users and enterprise clients.

The path ahead mixes opportunity with execution risk. On the upside, growing mobile-money penetration and accelerating intra-Africa commerce create a large addressable market for integrated wallets and payout APIs; Eversend’s focus on virtual accounts and card rails also opens higher-value revenue lines (receiving accounts, FX spreads, card fees). On the downside, scaling such services requires deep liquidity lines, robust AML/CFT and licensing in each market, plus margin management across volatile FX corridors. Success will hinge on the company’s ability to secure institutional liquidity, widen regulated payout licenses, and keep API reliability high for enterprise customers. If Eversend nails those operational challenges while maintaining low consumer fees, it could convert strong product fit into sustainable scale across Africa’s fragmented payments landscape.

7. Afriex – Nigeria

Afriex has quickly emerged as a major player in Africa’s cross-border remittance landscape, positioning itself as a seamless bridge for diaspora payments and intra-African transfers. Founded in 2019 and headquartered in Lagos, the platform enables users to send and receive money in local currencies while also offering dollar-denominated wallets to preserve value amid FX volatility. This dual-currency capability is especially appealing in markets like Nigeria, Ghana, and Kenya, where currency fluctuations can erode remittance value. According to fintech trackers, Afriex serves over 200,000 active users and is increasingly popular among freelancers, SMEs, and diaspora communities seeking low-cost, instant transfers to Africa. CEO Michael Fajolu has emphasized that Afriex’s mission is “to make global money movement as fast, transparent, and affordable as possible,” a goal that reflects the broader trend of tech-driven remittance solutions challenging traditional banks and money transfer operators.

Afriex’s product strategy leverages both consumer convenience and regulatory compliance to scale rapidly. The platform integrates with multiple local banking APIs and mobile money systems to enable real-time transfers across Nigeria, Ghana, Kenya, and Uganda. It also offers savings in USD, providing a hedge against currency depreciation, a feature that resonates strongly with expatriates and small businesses managing international cash flows. According to regional fintech analyses, Afriex is ranked among the top 15 African fintech startups by deal volume and funding momentum in 2025, reflecting growing investor confidence in its growth trajectory. The startup has also benefited from regulatory environments in Nigeria and Kenya that increasingly favor licensed digital financial services providers while protecting consumer funds.

Looking ahead, Afriex faces both opportunity and operational challenges. The African remittance market is projected to reach over $60 billion by 2026, driven by diaspora inflows and intra-continental trade, offering a large addressable market for Afriex’s dual-currency model. However, scaling requires navigating FX volatility, ensuring liquidity for instant payouts, and complying with evolving AML/CFT regulations across multiple jurisdictions. Afriex’s ability to maintain low fees, fast transfer speeds, and strong compliance will be critical to sustaining its competitive advantage. As Afriex continues expanding its wallet and remittance offerings, it is poised to cement its position as a leading African fintech for secure, cross-border dollar payments, empowering both individuals and businesses with a reliable alternative to traditional banking channels.

6. Mukuru – South Africa

Mukuru, headquartered in Johannesburg, South Africa, has established itself as one of the continent’s most trusted cross-border remittance providers, serving millions of users across Africa and beyond. Founded in 2004, Mukuru initially focused on facilitating low-cost, reliable remittances from the diaspora in Europe to Southern and Eastern Africa. Over the years, it has expanded its footprint to over 20 countries, including key corridors in Zimbabwe, Zambia, Malawi, and Mozambique. According to the World Bank’s remittance data, Mukuru processes over $2 billion annually, positioning it among the top African fintechs for cross-border transfers. CEO Parth Trivedi emphasizes that “Mukuru’s mission is to make sending money back home faster, more affordable, and transparent, giving people peace of mind while helping families thrive.” Its reputation for reliability and affordability has made it particularly appealing to migrant workers and expatriates who depend on remittances for household income.

Mukuru’s growth strategy combines digital innovation with a strong agent network across Africa. The platform leverages mobile money systems, bank integrations, and a network of cash payout points to ensure funds are accessible even in rural regions. Mukuru has also introduced digital wallets and bill payment solutions, providing users with more flexibility in managing their finances. According to regional fintech rankings, Mukuru is recognized not only for transaction volume but also for operational efficiency, low fees, and compliance with AML/CFT regulations. This focus on transparency and regulatory adherence has enabled Mukuru to secure partnerships with major international remittance operators and financial institutions, further boosting its credibility and reach.

Looking forward, Mukuru faces both opportunities and challenges in a rapidly evolving remittance landscape. Africa’s remittance market is projected to surpass $60 billion by 2026, driven by diaspora inflows, intra-African trade, and increasing digital adoption. Mukuru is well-positioned to capitalize on this trend, especially as mobile money penetration continues to rise in sub-Saharan Africa. However, competition from emerging fintech startups, FX volatility, and complex regulatory environments across multiple jurisdictions remain key challenges. Mukuru’s continued investment in digital infrastructure, user experience, and strategic partnerships will be critical to maintaining its market leadership. As Trivedi notes, “Our focus remains on empowering users with secure, instant, and affordable ways to send money home, no matter where they are,” reinforcing Mukuru’s commitment to bridging financial inclusion gaps across the continent.

5. Chipper Cash – Ghana

Chipper Cash, headquartered in Accra, Ghana, has emerged as one of Africa’s most dynamic cross-border payment platforms, serving millions of users across the continent. Founded in 2018 by Ham Serunjogi and Maijid Moujaled, Chipper Cash specializes in seamless peer-to-peer transfers, mobile money integration, and instant cross-border payments without hidden fees. According to a 2025 report by Disrupt Africa, the platform has facilitated over $6 billion in transactions across 10 African countries, including Ghana, Nigeria, Kenya, Uganda, and South Africa. Serunjogi emphasizes that “our mission is to democratize access to financial services in Africa by making money transfers simple, affordable, and instant.” Its user-friendly interface, combined with strong mobile penetration strategies, has positioned Chipper Cash as a household name among individuals, SMEs, and diaspora communities.

The company’s competitive edge lies in its robust technological infrastructure and strategic partnerships with local banks, mobile network operators, and fintech innovators. Chipper Cash allows users to link multiple wallets, transact in local currencies, and even invest in US stocks, creating a holistic financial ecosystem. According to fintech analyst reports, the platform processes hundreds of thousands of transactions daily, with an average transaction value ranging from $50 to $300. By integrating compliance measures such as KYC verification and real-time fraud detection, Chipper Cash maintains both regulatory credibility and user trust—a combination critical in Africa’s largely cash-driven economies. Its recognition alongside platforms like Sendwave and Eversend underscores its leadership in the continent’s cross-border remittance sector.

Looking ahead, Chipper Cash is leveraging its strong market position to expand into new corridors and financial products. With Africa’s remittance market expected to reach $60 billion by 2026, the startup is exploring opportunities in business-to-business payments, merchant services, and crypto-enabled transfers. Competition from both global players and emerging African fintechs remains intense, but Chipper Cash’s scale, brand recognition, and innovative product suite give it a significant advantage. As Ham Serunjogi notes, “The future of African fintech lies in creating platforms that are not just transactional, but transformative, enabling financial inclusion, entrepreneurship, and cross-border commerce.” With continued investment in technology and regional expansion, Chipper Cash is well-positioned to remain a central player in Africa’s remittance and digital finance ecosystem.

4. Wave – Senegal

Wave, headquartered in Dakar, Senegal, has rapidly risen to become one of Africa’s most influential fintechs, achieving a valuation of $1.7 billion in 2025 and cementing its position as a major player in mobile money and cross-border remittance services. Founded in 2018 by Derek Ting and Will Kwamba, Wave has grown to serve over 15 million users, capturing an estimated 70% of Senegal’s mobile money market. According to regional fintech reports, the startup processes more than $1 billion in monthly transactions, highlighting both the scale of its operations and the trust it has cultivated among users. Kwamba emphasizes, “Our goal is to make financial services as accessible and affordable as possible for everyday Africans, whether it’s sending money across town or across borders.” Wave’s rapid adoption is largely due to its low-fee model, seamless mobile experience, and strategic partnerships with telecom operators.

The company differentiates itself through a versatile ecosystem that extends beyond basic remittance services. In addition to peer-to-peer transfers, Wave offers bill payments, airtime top-ups, and innovative e-ticketing solutions for public transport and events. This integration of financial services with everyday needs has deepened user engagement and positioned Wave as more than a payments platform, it is becoming a central component of Senegalese daily life. Analysts note that Wave’s ecosystem-driven approach allows it to capture more transaction data, refine risk management, and offer tailored microloans and savings products, further embedding itself in the local economy. A 2025 report from FSD Africa underscores that such product diversification is key to maintaining market dominance, particularly in competitive mobile money landscapes across West Africa.

Looking ahead, Wave is expanding its footprint beyond Senegal into Côte d’Ivoire, Mali, and Guinea, targeting both diaspora and local users for cross-border remittances. With Africa’s total remittance inflows expected to surpass $70 billion by 2026, Wave’s strategic growth, technological innovation, and deep understanding of user behavior position it to capture a significant share of this market. Kwamba notes, “We’re focused on creating an ecosystem where users don’t just transact, they thrive. From payments to savings to credit, Wave aims to empower communities across the continent.” As global investors continue to pour capital into African fintechs, Wave’s combination of scale, innovation, and market trust ensures it remains a leading force in reshaping the remittance and mobile money landscape.

3. Sendwave – Pan-African

Sendwave, part of the US-based fintech group Zepz, has become a dominant force in the African remittance space, particularly for diaspora communities seeking fast, affordable transfers to family and businesses across the continent. The platform serves key markets including Kenya, Ghana, and Nigeria, with additional services expanding into Uganda, Tanzania, and Senegal. According to a 2025 report by Statista and regional fintech trackers, Sendwave processed over $3 billion in transactions in 2024 alone, illustrating both its scale and reliability. The startup’s appeal lies in its near-instant transfer capability to mobile wallets, minimal fees, and transparent exchange rates, a combination that has made it a preferred choice for millions of African expatriates. Industry analysts highlight that Sendwave’s diaspora-focused strategy not only captures remittance flows but also strengthens cross-border digital financial inclusion, fostering a broader adoption of mobile money solutions.

Zepz’s backing has been instrumental in Sendwave’s rapid growth. In 2024, the company closed a $267 million Series F funding round, led by international investors including TCV and Quona Capital, aiming to scale operations, enhance technology, and expand partnerships with African mobile money operators. Financial experts note that this level of capital injection enables Sendwave to maintain its competitive edge by offering near-zero latency transfers, robust fraud prevention measures, and seamless multi-currency transactions. CEO Xavier McNair of Sendwave stated, “Our mission is to make sending money home as effortless and cost-effective as possible. With this funding, we can further reduce friction for users and expand access to mobile money in every corner of Africa.” This investor confidence underscores the growing global recognition of Africa’s remittance market as a high-growth, impact-driven sector.

Beyond financial metrics, Sendwave’s strategic positioning highlights broader trends in African fintech: the integration of diaspora remittances with local mobile wallet ecosystems, the leveraging of advanced fraud detection and compliance frameworks, and the focus on user experience tailored to cross-border needs. The company has also partnered with NGOs and development finance institutions to promote financial literacy and inclusion, particularly among unbanked populations. Analysts from Finextra note that Sendwave’s approach demonstrates a model where international capital and local operational expertise converge to address Africa’s long-standing remittance inefficiencies. As the continent’s total formal remittance inflows are projected to exceed $70 billion by 2026, Sendwave’s continued innovation and diaspora-centric model position it as one of the most influential players shaping Africa’s digital financial landscape.

2. NALA – Tanzania / Nigeria

Founded in 2017, NALA has rapidly established itself as one of Africa’s leading digital remittance platforms, focusing on providing fast, low-cost transfers for diaspora communities sending money from the UK, US, and EU to the continent. Operating in 11 African countries, including Tanzania, Nigeria, Kenya, and Uganda, NALA leverages mobile money networks and banking partnerships to ensure near-instant transactions. According to a 2025 report by EconomyAfrica.com, NALA has processed over $1.5 billion in cross-border remittances since its inception, helping families and small businesses bypass traditional high-fee corridors. Its ease of use, combined with competitive foreign exchange rates, has made it particularly popular among younger, tech-savvy diaspora users who value transparency and speed. As NALA’s co-founder and CEO, Martin Mwakalebela, explains, “Our goal has always been to remove friction in sending money home. Every dollar saved on fees means more value for the recipient.”

NALA’s growth has been fueled by strong investor confidence, notably its $40 million Series A funding round, which closed in 2024 and included investors such as Accion Venture Lab, Flourish Ventures, and LocalGlobe. Analysts note that the Series A capital allows NALA to scale both technology infrastructure and regional operations, as well as explore additional services such as savings wallets, bill payments, and credit facilities for African users. The startup’s innovative approach includes AI-powered compliance checks, real-time FX updates, and fraud monitoring systems, ensuring that transfers are secure, transparent, and efficient. Data from TechCrunch Africa indicates that NALA’s customer retention rate exceeds 75%, a metric that underscores the platform’s reliability and strong brand loyalty in the competitive remittance market.

Beyond financial and technical growth, NALA’s impact on Africa’s digital finance ecosystem is significant. By reducing remittance costs, often by 50–70% compared to traditional banks—NALA is directly improving household incomes and supporting small business liquidity in recipient countries. In Tanzania and Nigeria, where mobile money adoption continues to rise, NALA has partnered with telecom operators and fintech incubators to promote financial literacy and expand access for underbanked populations. EconomyAfrica.com highlights that platforms like NALA not only streamline money flows but also serve as gateways to broader financial inclusion, enabling users to save, invest, and participate in the digital economy. As remittance volumes to Africa are projected to reach $80 billion by 2026, NALA’s scalable, tech-driven approach positions it as a transformative force in the continent’s cross-border payments landscape.

1. LemFi – Nigeria

LemFi, a fintech startup founded in 2020 by Ridwan Olalere and Rian Cochran, has rapidly emerged as a leading player in the remittance industry, particularly serving African immigrants. Headquartered in London with operations spanning across Europe, North America, and Africa, LemFi offers a platform that enables users to send money globally, open multi-currency accounts, and access financial services tailored to their needs. By early 2025, the company had onboarded over 1 million customers and was processing more than $1 billion in monthly transactions, marking a significant milestone in its growth trajectory.

In January 2025, LemFi secured $53 million in a Series B funding round led by Highland Europe, with participation from existing investors such as Left Lane Capital, Palm Drive Capital, and Y Combinator. This funding brought LemFi’s total capital raised to $85 million, underscoring investor confidence in its business model and growth prospects. The capital infusion is being utilized to scale operations, enhance technological infrastructure, and expand into new markets. Notably, LemFi has made strategic acquisitions, including a partnership with Modulr and the acquisition of a Republic of Ireland-based company, to facilitate its European expansion and establish independent operations in the region.

LemFi’s growth is further bolstered by its strong presence in the Asian remittance corridor, where it processes $160 million in monthly transactions, experiencing a 30% month-on-month growth. This success is attributed to the company’s robust fraud detection systems, competitive pricing, and localized services that cater to the unique needs of immigrant communities. With a team of over 300 employees across multiple continents, LemFi is poised to continue its expansion, aiming to provide seamless and affordable financial services to diaspora communities worldwide.

https://www.africanexponent.com/top-10-largest-money-remittance-startups-in-africa-2025/