In Summary

- Africa’s highest debt burdens are driven by pandemic recovery, climate shocks, and global inflation, forcing nations to borrow for essential imports and services.

- Countries like Zimbabwe and Sudan face ratios over 150%, with debt distress blocking IMF financing and requiring complex restructuring programs.

- Solutions hinge on IMF reforms, climate finance, and transparent governance to achieve fiscal stability amid austerity pressures and slow growth.

Deep Dive!!

Saturday, 08 November 2025 – The global economic environment of the mid-2020s presents a complex set of challenges, and African nations are navigating this terrain while carrying the heavy legacy of recent crises. The compounded effects of the COVID-19 pandemic, which strained public health systems and disrupted economic activity, have been followed by persistent global inflationary pressures and an increasing frequency of climate-related shocks. These sequential challenges have created a perfect storm, testing the fiscal resilience of economies across the continent and forcing difficult policy choices.

In response to these immense pressures, many governments have had to make a pragmatic yet perilous decision: accrue significant public debt to bridge critical financing gaps. This borrowing has been essential to maintain the import of vital goods, fund foundational social services, and continue investments in much-needed infrastructure. However, this has led to a rapid escalation of public debt levels, placing numerous countries in situations of high debt distress and forcing a delicate balancing act between immediate stability and long-term fiscal sustainability.

This article provides a critical analysis of this pressing issue by ranking the top ten African countries with the highest Debt-to-GDP ratios projected for 2025. Grounded in verified data and economic projections from the International Monetary Fund (IMF) and the World Bank, this ranking goes beyond the numbers to explore the root causes of each nation’s debt burden, the profound socio-economic impacts on their populations, and the ongoing domestic and international efforts, from IMF programs to the G20 Common Framework, being deployed to chart a path back toward fiscal stability and economic growth.

10. Ghana

Ghana’s debt-to-GDP ratio is projected to remain elevated near 85% in 2025, despite the landmark agreement reached with its official creditors under the G20 Common Framework. The country’s debt distress, which culminated in a domestic debt restructuring program in 2023, was triggered by a combination of large fiscal deficits, currency depreciation, and rising global interest rates. While the official creditor deal provides some fiscal breathing room, servicing the restructured debt still consumes a significant portion of government revenue.

The government, under its $3 billion IMF Extended Credit Facility program, is implementing stringent fiscal consolidation measures. These include new tax measures, cuts to energy sector subsidies, and efforts to bolster tax administration. As Finance Minister Mohammed Amin Adam stated, “We are committed to the reforms under the IMF program to restore macroeconomic stability and place our debt on a sustainable path.” The success of these measures hinges on maintaining political stability and achieving higher economic growth.

The long-term outlook for Ghana depends on its ability to leverage its natural resources, such as gold and cocoa, to boost exports and strengthen the cedi. Diversifying the economy away from primary commodities and improving public financial management are critical to avoiding future debt cycles. However, the nation remains vulnerable to external shocks, and its debt sustainability is fragile.

9. Zambia

Zambia is projected to have a debt-to-GDP ratio of approximately 88% in 2025, a figure that reflects the long and complex journey of its debt restructuring process. As the first African country to default during the pandemic era, it took years to finalize agreements with both private bondholders and official bilateral creditors, led by China and France. The resolution, while relieving immediate pressure, has left the country with a high debt stock that requires careful management.

The $1.3 billion IMF-supported program is the cornerstone of Zambia’s recovery strategy, focusing on fiscal discipline, domestic revenue mobilization, and pro-poor spending. The government is also working to reform its loss-making state-owned enterprises, particularly in the energy sector, which have been a major drain on public finances. An IMF review mission recently noted, “Zambia’s performance under the program is strong, but continued reform implementation is essential.”

Future prospects are cautiously optimistic. Zambia’s vast copper reserves position it to benefit from the global green energy transition. Attracting foreign direct investment into the mining sector and ensuring that mineral revenues are transparently managed are pivotal to generating the growth necessary to outpace its debt burden. The nation serves as a critical test case for the G20 Common Framework’s effectiveness.

8. Malawi

Malcolm’s economic outlook for 2025 remains challenging, with a debt-to-GDP ratio projected to exceed 90%. The country has been severely battered by climate shocks, including Cyclone Freddy in 2023 and subsequent droughts, which have devastated agricultural output, the backbone of the economy. This has led to a high dependency on foreign aid and concessional borrowing to fund food imports and basic services, further increasing the public debt stock.

A massive currency devaluation of over 40% in 2023 dramatically inflated the local currency value of its external debts, pushing the nation into debt distress. The government is engaged in negotiations with the IMF for a new financial arrangement and is seeking debt relief under the Common Framework. The Reserve Bank of Malawi Governor emphasized, “The path to recovery requires a combination of fiscal prudence, donor support, and, most critically, a recovery in our agricultural sector.”

The social impact is severe, with high inflation eroding purchasing power for millions. Malawi’s debt sustainability is intrinsically linked to its climate vulnerability. Accessing climate finance for resilient infrastructure and adopting climate-smart agriculture are not just developmental goals but essential strategies for debt management. The international community’s support is crucial to prevent a humanitarian crisis.

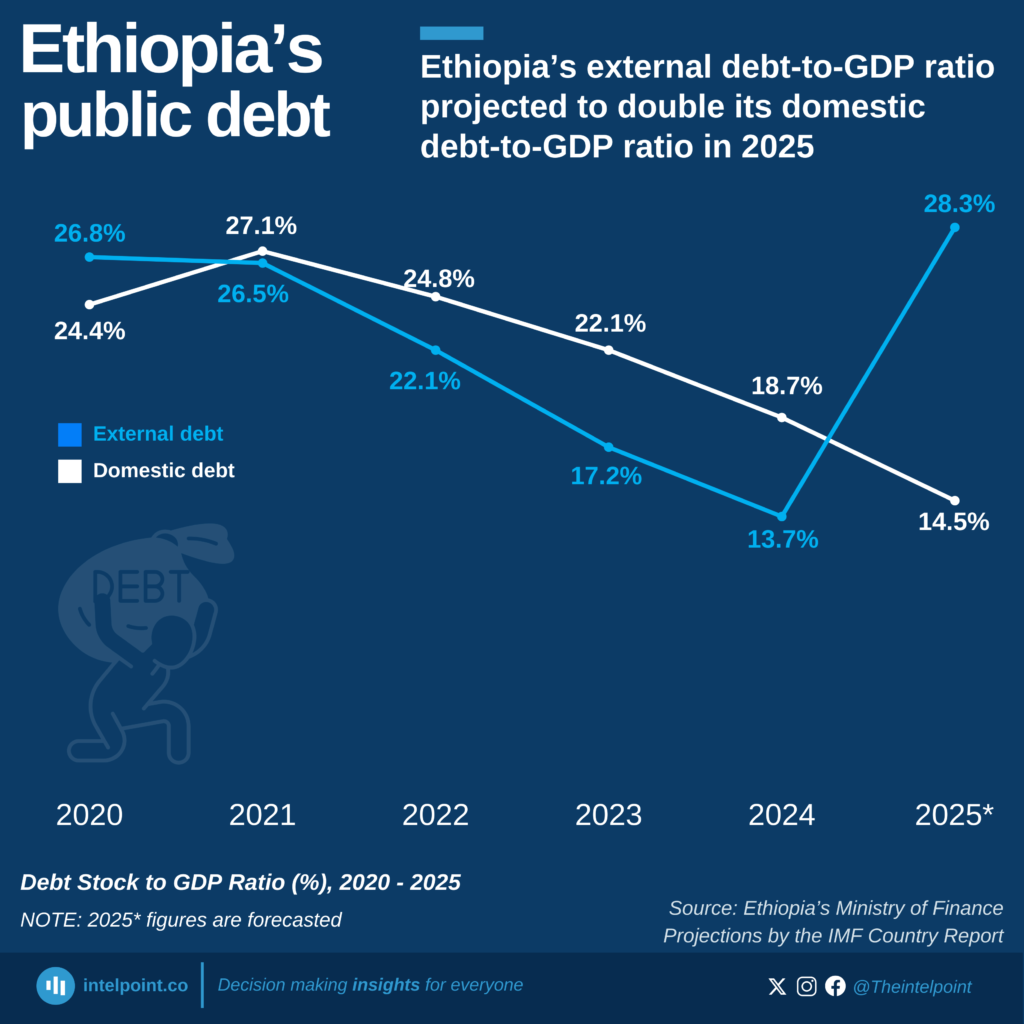

7. Ethiopia

Ethiopia’s debt-to-GDP is estimated to be around 92% in 2025, as it emerges from a period of conflict and engages in its own complex debt restructuring process. The country secured a preliminary agreement with bilateral creditors, but finalizing details with private creditors remains a key challenge. Years of high public investment in infrastructure, financed largely by external borrowing, have left the government with a substantial debt servicing burden.

The economy is undergoing a profound transition, moving from a state-led to a more market-oriented model under an IMF program. Key reforms include privatizing state-owned enterprises, liberalizing the telecommunications and financial sectors, and unifying the exchange rate. These measures are designed to attract foreign investment and spur growth. A World Bank report stated, “Ethiopia’s reform agenda is ambitious and holds the key to unlocking its significant economic potential.”

The ongoing recovery from a devastating civil war and severe drought complicates the fiscal picture. Ethiopia’s large population and strategic location offer significant growth potential, but political stability and the success of its peace process are fundamental prerequisites for economic recovery and sustainable debt management.

6. Mozambique

Mozambique’s debt-to-GDP ratio is forecast to stay high at about 95% in 2025. The country is still grappling with the aftermath of the hidden debt scandal of 2016, which led to a suspension of direct budget support from international partners. While the discovery and development of vast offshore natural gas fields promise a future revenue windfall, project delays and security insurgencies in the gas-rich Cabo Delgado province have postponed the fiscal benefits.

The government remains reliant on IMF support through an Extended Credit Facility, which focuses on improving governance, strengthening public financial management, and enhancing transparencyc, especially in the management of future natural resource revenues. A senior IMF official commented, “Mozambique’s challenge is to bridge the fiscal gap until LNG revenues materialize, without accumulating further unsustainable debt.”

The long-term outlook hinges on stabilizing the security situation and successfully bringing the LNG projects to production. When operational, these projects could transform the economy and drastically improve debt sustainability. However, in the short term, the population continues to bear the burden of austerity measures and high living costs.

5. Eritrea

Eritrea maintains one of the continent’s most opaque economies, with a projected debt-to-GDP ratio estimated by analysts to be around 165%. The country’s debt is primarily held by bilateral creditors, and its economic policy is dominated by national service and a state-controlled system that stifles private enterprise. A significant portion of its debt is related to military spending and the border conflict with Ethiopia.

The lack of engagement with international financial institutions like the IMF or World Bank means there is no formal program to address debt sustainability. The government operates in isolation, and the debt burden is effectively managed by simply not servicing a large portion of it, which further limits its access to external financing. This isolation has crippled the formal economy and led to high levels of emigration.

The potential for debt resolution is low without a fundamental shift in political and economic governance. Any future normalization of relations with the international community would likely involve a complex and politically charged debt restructuring process. For now, the debt remains a stagnant, unresolved burden on the nation’s development prospects.

4. Cape Verde

Cape Verde’s debt-to-GDP is projected to be among the highest in the world at approximately 170% in 2025. As a small island developing state with limited natural resources, its economy is highly dependent on tourism. The COVID-19 pandemic caused a profound economic shock, wiping out its primary source of revenue and forcing a sharp increase in public borrowing to support the economy and fund essential imports.

The country is classified as being at high risk of debt distress. The government is pursuing an IMF-supported program focused on fiscal consolidation and promoting a resilient and inclusive recovery. Key measures include improving the efficiency of public investment and strengthening financial sector supervision. The Prime Minister, Ulisses Correia e Silva, has acknowledged, “Our debt is a reflection of our vulnerability. We need a global partnership that recognizes the unique challenges of SIDS.”

Cape Verde’s case highlights the plight of Small Island Developing States (SIDS) facing climate change and economic remoteness. The international community is discussing specialized support for such nations, including more concessional financing and climate-resilient debt clauses, which would pause debt payments following a natural disaster.

3. Sudan

Sudan faces a catastrophic economic situation, with a debt-to-GDP ratio projected to be well over 150% in 2025. The ongoing civil war has decimated the economy, destroyed infrastructure, and displaced millions. Government revenue collection has collapsed, and public finances are directed almost entirely toward conflict, leaving essential services and debt payments unfunded.

The country has accumulated significant arrears to international financial institutions, making it ineligible for new financing and debt relief programs. Before the conflict, there were discussions about debt relief under the Heavily Indebted Poor Countries (HIPC) Initiative, but these are now suspended indefinitely. A UN development report bleakly concluded, “The resolution of Sudan’s debt crisis is entirely contingent upon a durable peace agreement.”

The humanitarian crisis is the immediate priority. Rebuilding the economy and addressing the debt overhang will be a monumental task that can only begin after a political settlement is reached. The international community will likely need to consider a comprehensive debt forgiveness package post-conflict to give the nation a fresh start.

2. Republic of Congo

The Republic of Congo’s debt-to-GDP ratio is projected to be around 110% in 2025. The country’s finances are overwhelmingly dependent on oil revenues, making them highly volatile. A period of low oil prices prior to 2022 led to a rapid accumulation of debt, including from commodity-backed loans with non-Paris Club creditors, which often carry less favorable terms.

The country reached a debt restructuring agreement with the Paris Club and other creditors and is under an IMF program. The government is attempting to diversify the economy and improve the management of its oil revenues, but progress has been slow. Governance challenges and a reliance on a single commodity continue to pose significant risks.

While higher oil prices provide temporary relief, they do not solve the structural issues. Sustainable debt management will require breaking the cycle of oil dependency, improving transparency in the hydrocarbons sector, and investing oil revenues into sectors that can generate more broad-based economic growth and jobs.

1. Zimbabwe

Zimbabwe is projected to have the highest debt-to-GDP ratio in Africa in 2025, estimated at over 200% when including both acknowledged and contingent liabilities. The debt is largely in arrears, meaning the government is not making current payments, which blocks access to fresh financing from IFIs. This debt overhang is a major barrier to economic recovery and infrastructure development.

The government has launched a structured Arrears Clearance and Debt Resolution process, led by former African Development Bank President Dr. Akinwumi Adesina. This involves engaging with international creditors to negotiate a roadmap for clearing arrears and securing debt relief. Dr. Adesina has described the situation as “a burden that has constrained Zimbabwe’s potential for far too long.”

The resolution of Zimbabwe’s debt crisis is fundamentally political, linked to the implementation of comprehensive economic and governance reforms, particularly regarding land ownership and compensation. Until a credible and transparent resolution path is agreed upon with international partners, the colossal debt burden will continue to stifle investment and perpetuate economic instability for its citizens.

We welcome your feedback. Kindly direct any comments or observations regarding this article to our Editor-in-Chief at [email protected], with a copy to [email protected].

https://www.africanexponent.com/top-10-african-countries-with-the-highest-debt-to-gdp-ratios-in-2025/