In Summary

- Ham Serunjogi represented Uganda in swimming at the 2010 Youth Olympic Games before turning to fintech leadership.

- After earning a degree in economics in the United States, he worked at Meta in Dublin, gaining experience in tech and payments, before co-founding Chipper Cash, which targets African markets.

- Under his leadership, the company raised successive VC rounds, achieved unicorn status (valuation over US$1-2 billion), built a multi-country footprint, and expanded product lines beyond P2P transfers.

Deep Dive!!

Lagos, Nigeria, Tuesday, November 4 – Ham Serunjogi is the co-founder and Chief Executive Officer of Chipper Cash, a pan-African fintech company that provides seamless cross-border and domestic payment solutions, digital merchant services, and investment tools. Established in 2018, the company was born out of a vision to solve one of Africa’s most persistent challenges, expensive and fragmented financial transactions across national borders.

Initially focused on peer-to-peer transfers, Chipper Cash has since expanded its offerings to include merchant payments, cryptocurrency trading, and stock investments, positioning itself as a comprehensive digital financial platform across the continent.

Though its headquarters are in San Francisco, Chipper Cash remains profoundly African in origin, leadership, and market focus. The company operates in over seven African countries, including Nigeria, Ghana, Uganda, South Africa, Kenya, Tanzania, and Rwanda, and its services also extend to diaspora users in the United States and the United Kingdom.

Chipper Cash’s mission is rooted in financial inclusion, offering individuals and businesses an alternative to traditional banking systems that are often slow, costly, and limited by borders. Its platform enables users to send and receive funds instantly, pay for goods and services, and access investment opportunities without the friction of conventional remittance channels.

Under Serunjogi’s leadership, Chipper Cash has achieved rapid growth and market recognition. The company has raised over $300 million from international investors, including Ribbit Capital, Deciens Capital, and Bezos Expeditions, achieving a valuation above $2 billion and joining the ranks of Africa’s first fintech unicorns.

Beyond capital, the company has expanded its operational footprint, built a robust technology infrastructure, and scaled to millions of monthly active users. Its success reflects a pan-African vision that bridges domestic and diaspora markets, integrating financial systems across multiple jurisdictions while maintaining a distinctly African identity.

Serunjogi’s personal journey mirrors the scale and ambition of Chipper Cash. A former competitive swimmer who represented Uganda at the 2010 Youth Olympic Games, he cultivated discipline, international exposure, and a global perspective from an early age.

This article explores how Ham Serunjogi’s education, international experience, and entrepreneurial vision combined to create Chipper Cash, a fintech company that is reshaping payments, enabling financial inclusion, and connecting Africa’s digital economy to the world. It traces the origins, growth, and milestones of the company, offering insights for entrepreneurs seeking to build scalable, pan-African businesses with global relevance.

Early Life, Education & Experience

Ham Serunjogi was born in December 1993 in Gayaza, a suburb of Kampala, Uganda. He grew up in a family that combined entrepreneurial initiative with a strong focus on education. His father ran an IT-services business serving local companies, while his mother ensured Ham and his siblings had a disciplined academic environment. From a young age, Ham displayed remarkable focus and drive and began competitive swimming at the age of six. This early commitment to sport instilled discipline, time management, and resilience, qualities that would later define his entrepreneurial journey.

By 16, Serunjogi had earned a place on Uganda’s swimming team for the 2010 Youth Olympic Games in Singapore. Representing his country on an international stage provided him with global exposure and taught him how to navigate high-pressure situations. At the same time, he experienced firsthand the limitations of African financial systems, as his father often had to travel across borders with cash to pay for Ham’s training abroad. This challenge would later inspire the vision behind Chipper Cash.

After the Youth Olympics, Ham received a scholarship to attend the Aga Khan Academy in Mombasa, Kenya. The Academy is known for rigorous academics, leadership training, and a focus on service and problem-solving. At AKA Mombasa, Ham excelled both in the classroom and in extracurricular activities, becoming President of the Student Representative Council. He continued to train and compete in swimming, overcoming injuries and demonstrating perseverance. The Academy’s emphasis on holistic development, community engagement, and global thinking profoundly shaped his approach to leadership and problem-solving.

After completing secondary school, Ham moved to the United States to study economics at Grinnell College in Iowa, where he enrolled from 2012 to 2016. He balanced academics with varsity swimming, student government, and technology projects. As treasurer of the Student Government Association, he managed budgets and operations, while also co-developing a mobile app that allowed encrypted voice messaging. This early initiative reflected his interest in using technology to solve communication and infrastructure gaps.

Upon graduation, Ham joined Meta Platforms, formerly Facebook, in Dublin, Ireland, where he managed partnerships with major UK advertisers. This role gave him direct experience with large-scale digital platforms, payments infrastructure, and cross-border business operations. The position honed his understanding of technology-driven business solutions, global market dynamics, and financial systems, skills that would become crucial when he co-founded Chipper Cash.

Serunjogi’s early life and education combined three interwoven threads: high-level competitive sports, which built discipline and global perspective; international schooling, which fostered leadership, problem-solving, and a pan-African worldview; and professional experience in tech and digital payments, which provided operational knowledge of scaling platforms. Together, these experiences laid the foundation for his vision and capability to create Chipper Cash, a company designed to address real financial challenges across Africa and its diaspora.

Inspiration to Start Chipper Cash

The idea for Chipper Cash emerged from Ham Serunjogi’s personal experiences growing up in Uganda and navigating the fragmented financial systems of Africa. One defining memory involved his father, who had to travel from Uganda to South Africa to pay for a training camp because local banking systems and cross-border payment channels were inefficient, costly, or simply unavailable. This early encounter with the limitations of African financial infrastructure left a lasting impression on Serunjogi and shaped his thinking about the continent’s economic challenges.

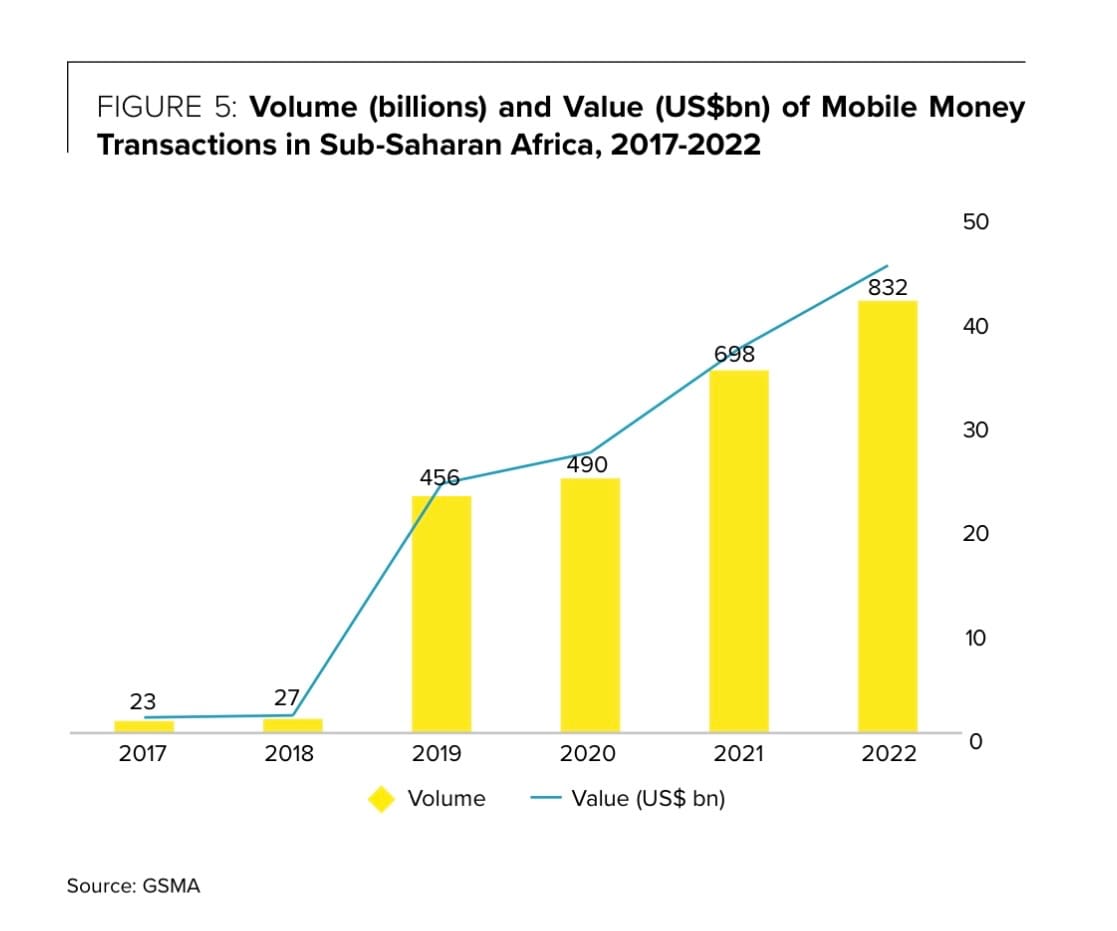

Later, while studying economics at Grinnell College in the United States, Serunjogi encountered additional frustrations that fueled the vision for Chipper Cash. He and co-founder Maijid Moujaled realized that even with modern technology, sending money across African borders was slow, expensive, and cumbersome. Global remittance providers charged high fees, and most solutions were designed for Western markets rather than African realities, which include more than 50 different currencies, multiple regulatory regimes, and inconsistent digital infrastructure. This fragmentation inspired Serunjogi to create a system tailored specifically for Africa. In 2019, Sub-Saharan Africa received an estimated $47-$48 billion in remittances. Advanced economies were the largest sources of these inflows, with the United States, the United Kingdom, France, and Italy among the major contributors. Even though the volume of money transfers from abroad is large, the cost of sending them remains high. For example, in Sub-Saharan Africa, the average cost of sending a typical remittance was around 8-9%, far above the UN’s target of less than 3% by 2030. Serunjogi and Moujaled recognized a clear opportunity how they can leverage technology to create a faster, cheaper, and more accessible alternative that served both domestic and diaspora users.

Serunjogi’s professional experience also contributed to the vision. While working at Meta Platforms in Dublin, he gained firsthand exposure to digital payments, large-scale platform operations, and partnerships with major advertisers. This background provided him with the skills and confidence to design scalable, secure financial solutions. He understood that building a pan-African fintech required not only technological innovation but also careful navigation of regulatory landscapes, cross-border compliance, and user trust insights he carried into Chipper Cash.

Chipper Cash was thus born out of a convergence of personal experience, professional insight, and market opportunity. Serunjogi has emphasized that the company was not just about facilitating transactions but about enabling financial inclusion across a continent where millions remain unbanked or underserved. From its inception, Chipper Cash aimed to reduce friction in payments, empower individuals and small businesses, and create a platform capable of expanding across multiple African countries and into global markets.

In essence, the inspiration for Chipper Cash combined lived experience, a deep understanding of Africa’s financial gaps, and the ambition to create a solution that could scale continent-wide. Serunjogi’s journey illustrates how personal insight, reinforced by professional expertise and market data, can catalyze transformative innovation in African fintech.

What Problem Chipper Cash Solves

At its core, Chipper Cash was built to tackle some of Africa’s most persistent financial challenges like high-cost cross-border payments, lack of banking access, and fragmented financial infrastructure that limit economic growth and inclusion.

1. High-Cost and Slow Cross-Border PaymentsBefore Chipper Cash entered the market, cross-border transfers in Africa frequently carried fees of around 7–10% and could take days. Chipper Cash introduced a service offering transfers in many corridors with minimal fees (in some cases no charge when both sender and recipient use the app) and faster delivery, making cross-border payments more accessible.

2. Limited Access to Banking for Individuals and SMEsMillions of Africans remain unbanked or underbanked, particularly in the informal sector. Over 350 million adults in Sub-Saharan Africa do not have access to traditional banking services. Chipper Cash allows individuals and small businesses to send, receive, and store funds without requiring a bank account, effectively democratizing financial access across multiple countries.

3. Fragmented Financial InfrastructureAfrica’s diverse currencies, regulatory environments, and digital ecosystems made payments and trade complex and inconsistent. Chipper Cash integrates multiple payment networks, mobile wallets, and banking rails to enable seamless domestic and cross-border transactions, creating a unified platform across otherwise fragmented financial systems.

4. Unreliable Payment SystemsTransaction failures and downtime were common in existing payment systems, eroding trust in digital solutions. Chipper Cash developed a resilient transaction infrastructure with redundant routing and localized servicing, achieving high uptime and reliability that users and merchants can depend on.

5. Lack of Access to Credit for SMEsSmall businesses and informal merchants often struggled to obtain working capital due to insufficient data for credit assessments. Chipper Cash uses real-time transaction histories and digital footprints to evaluate creditworthiness, providing loans that empower merchants to restock, expand, and scale their operations.

6. Fragmented Financial ManagementBeyond payments, many small enterprises lacked tools to manage bookkeeping, payroll, and finances. Chipper Cash offers integrated dashboards that allow merchants to track revenues, monitor expenses, and digitize operations, laying the foundation for formalized, sustainable business growth.

Since its launch in 2018, Chipper Cash has addressed these gaps across seven African countries, processing billions of dollars in transactions annually and enabling financial inclusion for millions. By combining technology, accessibility, and affordability, the platform demonstrates how fintech can overcome systemic barriers to economic participation on the continent.

Milestones Achieved To-Date

Chipper Cash launched in 2018, founded by Ham Serunjogi and Maijid Moujaled, with a simple, continent-wide objective to make domestic and cross-border transfers between African countries fast, inexpensive, and mobile-first. In its first year, the product rolled out across multiple East and West African corridors notably Uganda, Kenya, Rwanda, Ghana, and Nigeria proving demand for near-instant intra-African transfers and validating the thesis that a pan-continental payments layer could scale.

The company’s earliest institutional backing began in 2019 and crystallized in 2020. In mid-2020 Chipper closed a Series A round of approximately US$13.8 million, led by Deciens Capital (with participation from other early-stage funds). This capital funds engineering hires, compliance work, and market expansion. Later that same year, in November 2020, Chipper closed a Series B round of about US$30 million, led by Ribbit Capital with participation from Bezos Expeditions. The Series B accelerated country launches, product hardening, and the start of card capabilities.

Fundraising continued into 2021 with a major step to a US$100 million Series C announced in mid-2021 that brought blue-chip investors into the cap table and enabled expansion of product offerings beyond P2P transfers. That pivot was made explicit later that year when the company raised a US$150 million extension of the Series C in November 2021. The combined capital from the Series C and its extension pushed total disclosed funding past the US$300 million mark and, at the time, placed Chipper Cash among Africa’s unicorns with a post-money valuation reported slightly above US$2 billion. Different trackers later reported cumulative funding in the US$300–342 million range depending on cut-off dates and whether small seed checks were included.

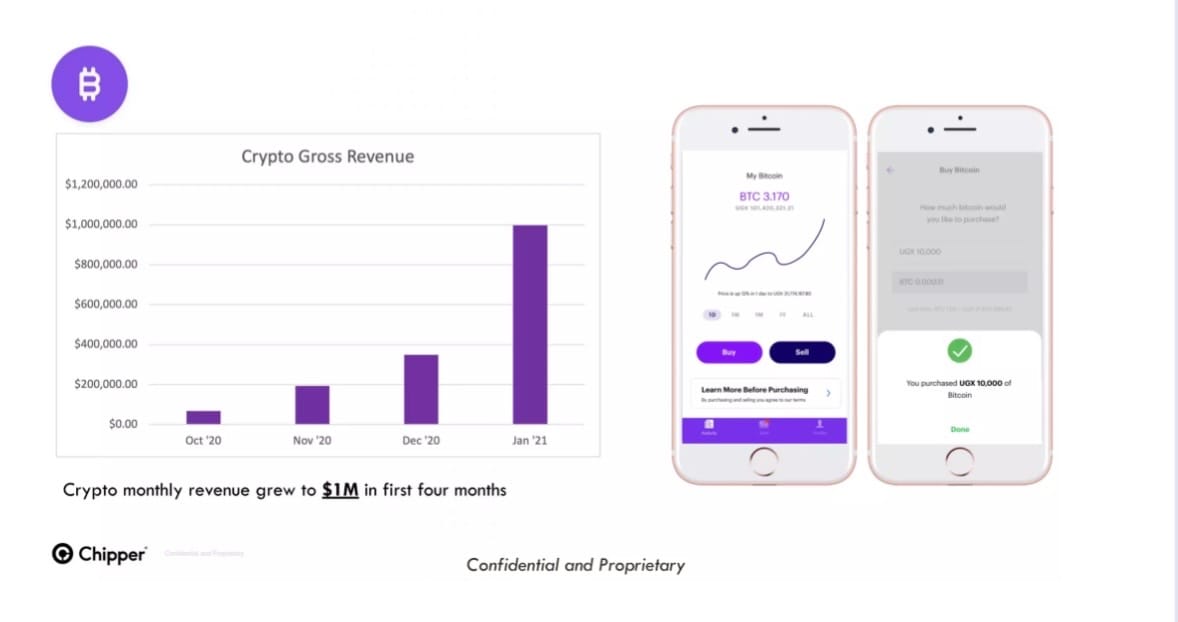

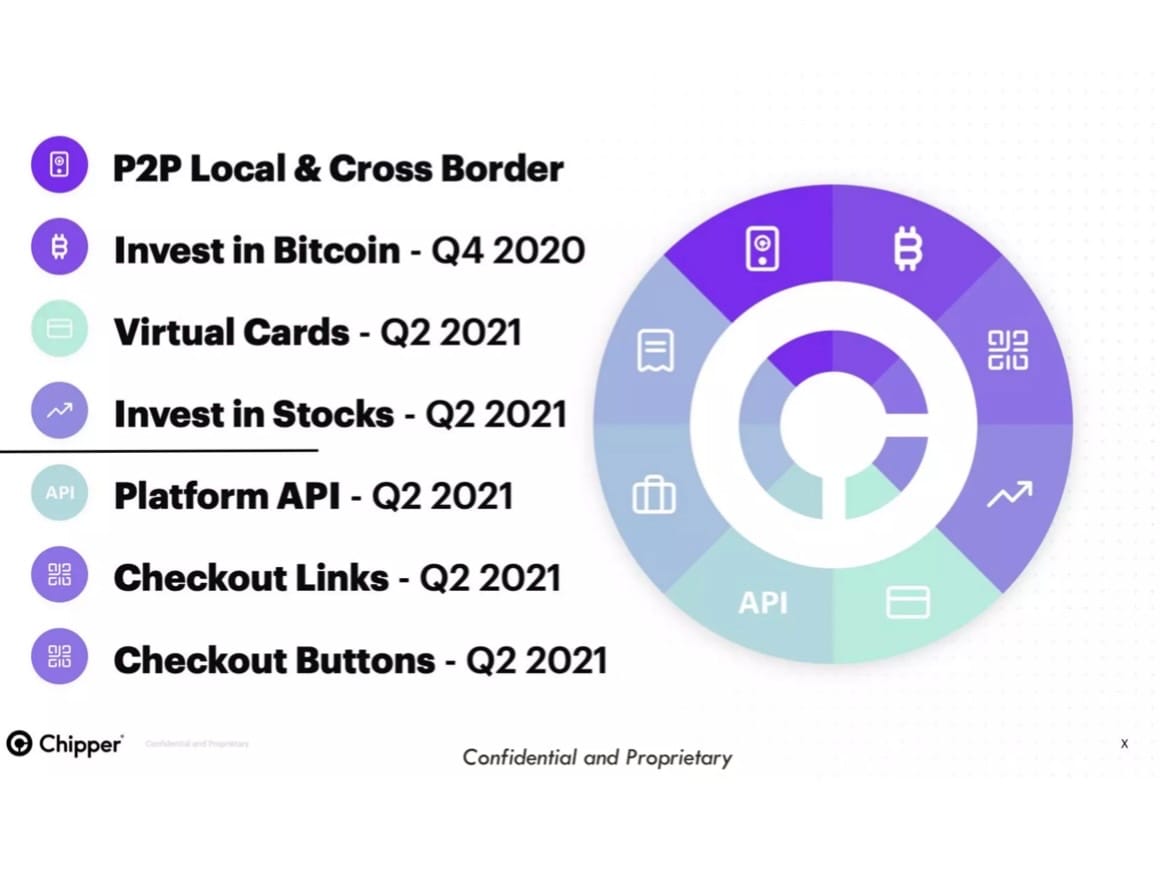

With that capital, Chipper moved quickly from a single-product remittance app to a multi-product fintech. From 2021 into 2022 the company launched the Chipper Card (virtual and limited physical issuance), merchant payment rails, a stocks investing product that enabled fractional share purchases of major US equities, and crypto on-ramps/settlement capabilities. The investing product attracted tens of thousands of new user accounts in its early months and produced measurable trading activity and the Chipper Card scale accelerated through 2022 and 2023 as the card product became a core monetisation channel.

According to company and third-party sources, Chipper Cash exceeded US$100 million in payment volume per month around 2020. By Q1 2022 one report cited a payment-volume figure of approximately US$1.65 billion (implying annualised volume of ~US$6.6 billion) though the source is not independently audited. While exact TPV numbers for later years are not publicly filed, the company reports serving over five million customers and having issued more than one million cards by late 2023.

Geographic and corridor expansion matched product breadth. Beyond its core African markets, Chipper opened diaspora corridors (U.S.–Africa, U.K.–Africa) to enable remittances into local African markets and to capture diaspora remittance flows. That expansion reinforced Chipper’s positioning as both Pan-African and globally connected. Strategic commercial partnerships including network partnerships to enable wider card acceptance and infrastructure collaborations aimed at faster settlement became central to the business model as the company moved toward embedded finance.

After its peak fundraising phase, Chipper Cash entered a tougher macro-funding environment in 2022 and 2023 and responded with cost reductions. The company had grown its workforce significantly during the scale-up period, and by 2023 it carried out multiple rounds of layoffs that affected over 100 roles and in one wave nearly a third of staff. Around the same period, investor materials indicated a valuation adjustment from the roughly US$2 billion level reported in 2021 to approximately US$1.25 billion in late 2022, reflecting broader global fintech repricing rather than company-specific collapse.

These changes mirrored broader fintech market corrections and positioned the company to focus more tightly on core markets, product monetisation, and sustainable unit economics.

On the technology and infrastructure front, Chipper invested in redundancy and multi-rail settlement to improve uptime and reduce failure rates. This included exploring crypto-enabled settlement rails to lower corridor costs and settlement times. A material signal of that approach was the March 2025 partnership with Ripple, announced to leverage Ripple’s payment rails and crypto-enabled liquidity for faster, lower-cost cross-border settlement across African corridors.

Throughout this period Chipper continued to attract strategic investors and partners that validated its multi-product strategy. The company’s funding history, product launches (cards, investing, merchant services, crypto rails), diaspora corridor creation, rapid user adoption, and operational retrenchment during the fintech market correction together form a complete arc of rapid scale driven by product expansion and capital, followed by consolidation and operational focus aimed at achieving durable unit economics. The milestones reflect both Chipper Cash’s concrete achievements and the broader structural realities of scaling pan-African fintech into capital intensity, regulatory complexity, corridor liquidity challenges, and the need to balance low-fee user value with sustainable revenue streams.

Lessons for Other Entrepreneurs

1. Solve lived problems before abstract ones

Ham Serunjogi’s upbringing between Uganda and the United States exposed him to the gaps in African financial access long before Chipper existed. Early experiences with cross-border difficulties and remittance frictions shaped his view that Africa’s economic future required frictionless movement of value across borders. Chipper Cash was not built as a “fintech idea” but as a response to personal and continental financial barriers. For African founders, deep familiarity with the problem often precedes durable innovation.

2. Pan-African infrastructure over single-market dominance

Chipper Cash launched simultaneously in multiple African markets, treating Africa as a unified economic zone rather than a sequence of isolated territories. With operations across East, West, and Southern Africa and later global corridors, the company demonstrated that African fintech scale depends on cross-market interoperability, regulatory navigation, and liquidity planning from day one. Entrepreneurs building continental solutions must architect technology and compliance frameworks for Africa’s fragmented financial rails instead of expanding reactively.

3. Strategic capital over spotlight capital

Chipper’s early rounds were led by investors with deep payments DNA, including Deciens Capital and Ribbit Capital, followed by participation from Bezos Expeditions. They were infrastructure-focused funds with experience in treasury, compliance, and settlement systems. African founders can draw from this that capital aligned with the technical and regulatory complexity of African markets matters more than capital that brings media attention but no strategic depth.

4. Sequenced product expansion grounded in trust

Chipper built trust with core P2P payments before expanding into cards, stock investing, and crypto rails. Each product layer sat on validated user behavior and infrastructure maturity. This order allowed adoption at scale without compromising regulatory posture or customer confidence. In a market where over-extension is common, this shows African fintechs benefit from measured sequencing grounded in operational readiness rather than marketing ambition.

5. Diaspora corridors as a foundational liquidity engine

Instead of treating international remittance flows as an add-on, Chipper positioned U.S.–Africa and U.K.–Africa corridors as central to its strategy. This unlocked deeper FX liquidity and remittance volumes, mirroring the financial reality that African economies are globally tethered through diaspora capital. Founders should recognize that Africa’s economic network is global and that scalable fintech must integrate diaspora rails early.

6. Market discipline as a survival advantage

Chipper’s layoffs and expense restructuring during the global fintech correction were not signs of failure but of operational maturity. As the market shifted, the company focused on treasury strength, unit economics, and long-term product sustainability. African founders should note that scale requires flexibility: rapid expansion during capital abundance and disciplined operational tightening during macro shifts.

7. Infrastructure innovation includes alternative rails

The company’s move toward crypto-enabled cross-border settlement and its partnership with Ripple in 2025 underline a key lesson that Africa’s settlement challenges demand hybrid models. With fragmented banking systems and high FX frictions, Chipper showed the importance of exploring alternative rails to reduce settlement time and cost. African fintechs should treat emerging financial rails as infrastructure opportunities, not speculative trends.

We welcome your feedback. Kindly direct any comments or observations regarding this article to our Editor-in-Chief at [email protected], with a copy to [email protected].

https://www.africanexponent.com/how-ham-serunjogi-built-chipper-cash-into-one-of-africas-leading-payments-platforms/